Myself, I’m more than a little torn on the issue. On the one hand, I naturally rebel against a company trying to lock down content that I’m going to pay for (not that that’s a concern with this specific case of a wrestling game). Being able to own something and resell it has been a long-standing property right, whether it’s a car, air conditioner*, book, or video game. Who is this greedy corporation to arbitrarily decide to degrade the product/service you paid for, just because you sold it on to someone else? Indeed, if it wasn’t for Blizzard making StarCraft2 impossible to transfer to a new account, my SC2 woes would have been solved in a trivial way. Heck, even if you twist it so that instead of “buying” a game, you “license” or “lease” one, in the real world even licensees and leasees can often assign or sublet.

On the other hand, I do want to support the ability of people to come together to trade money for stuff in ways that work for them. And digital delivery is going tomay require a different playbook than we’re familiar with from physical media.

Where I get caught up though, is when companies try to charge the same for less. If I can ordinarily share my games with friends when I’m done with them, or sell them used for $10, then this crippled version of the game should cost less up front because it is in fact an inferior product. Likewise with ebooks: there’s no reason in my mind for them to cost nearly as much as a paperback, and that’s from my point of view of receiving value, not even taking into account their lowered distribution/publishing costs side of things. So when these companies say that they don’t care about used buyers because they don’t (directly) see any of the money from the used transaction, I have to step up and say that they did get money from the used buyer, and they got it up front: the first buyer paid $50 for their own use of the game, and another $10 that they hope to get from the used buyer down the road.

* – incidentally, I’m still trying to sell my wall/slot air conditioner. If you’re London and want a used air conditioner for a wall slot (typically found in highrise apartments) send me an email!

I’ve been super busy lately, and I’ve shifted my leisure habits from blogging, writing, and finance lately to playing StarCraft and fiddling with Flash animations (which had even fewer views than I had suspected, and zero comments… I guess I only find myself funny because I’m sleep deprived?).

Anyhow, this picture should give you an idea of how the diet has been going this week:

Ok, actually it wasn’t all that bad. I did get back on the bike, and aside from the last day of cookies (and tomorrow’s chocolate party), I have been pretty good with the diet. I caught up on my sleep over the weekend, which also helped a lot with feeling better and getting a workout in. However, according to my “aggressive yet totally doable thesis timeline” I was supposed to defend my thesis last week. As you have not seen a post to that effect (or even that I’ve finished the first draft of my thesis), you know that I didn’t defend my thesis last week. That made me sad, and cookies are good friends when you’re in your little box of sadness.

Despite the recent spate of results coming out of so many companies, I haven’t had time to go over any of them in any kind of detail, and haven’t listened to a single conference call this quarter. So I’m not really in much of a position to come up with any good investing posts, but that won’t stop me from spewing out a few half-baked thoughts in this quasi-weekly roundup:

BP: They capped the well, the stock recovered very nicely from the bottom… and then the stock went down and down and down again. I have no idea why. I’m ambivalent on it at this price: it’s not cheap enough to be interesting for me to buy more, but especially with the well capped so the liability is no longer infinite, I wouldn’t want to bail at this point…

DR.UN: Medical Facilities is a neat little income trust that I flagged a few months ago as one to watch for the next quarter or two to see how things go. They got really cheap there for a while, yielding up around 15% (which would likely become a ~11% dividend after conversion). I skimmed their quarterly release and things looked ok — not great, but ok — but I didn’t have time to really read it in detail. They’ve since gone up about 10%, and I’m no longer sure how much of the value is there…

The Banks: the Canadian housing market looks like it’s finally following the rest of the world back down to reality. Now, the Canadian banks have very little risk of complete loss associated with that event, but I doubt very much that even the CMHC makes the risk zero. AFAIK, they will at the very least face a reduction in their mortgage portfolios as the number of Canadian homeowners follows the American trajectory from ~69% back to the historical ~64%, and the sizes of those associated loans shrink. Once the downturn gets into full swing, they’ll probably have a few bad quarters/years until things shake out. So even though they already are starting to look cheap again, I’ve been sitting on my hands on the assumption that they’ll get cheaper in the next few years. Unfortunately, I suppose that could be described as fruitless market timing, and that this idea is already baked into the prices… that said I do still have some exposure to Canadian banks (I still hold TD), though I think I’m slightly underweight compared to the index.

Conversely, the American banks may have hit bottom already. BAC is making the top picks of several analysts, but I haven’t had time to do any research to see if it might be fore me… likewise Manulife has been getting cheaper by the day, yet again, I can’t say yet if it’s cheap enough. With these though, I’m not sure I’d ever be able to — these entities are just so big, with so many moving parts and black boxes, I don’t think I could ever fully get my head around them with the skills and tools I have at my disposal right now.

Links:

An interesting article on how scarce helium is on our planet, and how a bone-headed move by the US government is causing a large part of our reserves to be sold off at rock-bottom prices, making helium too cheap to bother recycling… for now. To be fair, we can manufacture helium from nuclear processes, but not in large quantities, and certainly not cheaply.

It’s a concept book: it’s not going to tell you how to better manage your money or anything of the sort. There aren’t a lot of concrete examples, either. However, it discusses a number of important concepts, especially the important ways that we model the markets differ from reality. Models are of course important for being able to manipulate variables, to try to forecast the future, or to simplify things to get a better understanding. However, relying too much on models that are not accurate can bite us in the ass. “Clouds are not spheres, mountains are not cones, coastlines are not circles, and bark is not smooth, nor does lightning travel in a straight line.”

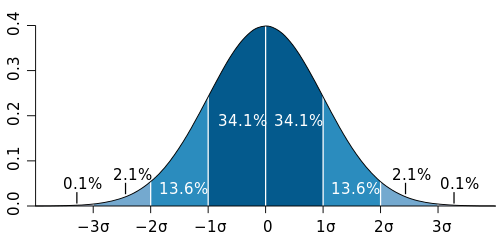

First, a quick bit in the way of introduction for those that don’t have a strong stats background. The Gaussian, or normal distribution is one that appears in a lot of places in nature (so much so that we call it the “normal” one!), even if you’re not very familiar with it, you must have seen the familiar bell-curve shape:

It looks a little different for every group of things you choose to measure. For instance, the lengths of pencils in a fresh box may have a very “sharp” bell curve, since each one is very nearly identical in length, varying by just fractions of a millimetre. The heights of adults in the population will be a bit wider, with some people towering head and shoulders above others. The heights of kids in a school may have a wider one yet, with some being young, some passing through their growth spurt. But for all these disparate measurements, you can describe the way their bell curve looks with just two numbers: the mean, and the standard deviation (σ). The mean tells you where the centre of the curve is, and the standard deviation how wide it is.

A lot of work has gone into investigating and characterizing these distributions. A very large part of the whole field of statistics is based on manipulating the properties of the normal distribution. There are countless tools out there to help you simulate or analyze data based on normal distributions. In addition to being common, the math is also fairly well-behaved, lending itself to analytical as well as numerical approaches.

So it may be no surprise then that a great number of tools exist for financial matters based on gaussian distributions. For example, if you go to a retirement planner, and they have a fancy program that will show you the various possible outcomes for how much money you’ll have to retire on based on how much you save, saying things like “95% of the time, you’ll have at least $X available per year until you turn 100” — those software tools are based on simulating possible market outcomes with this math. Options traders have formulas to tell them how much their derivatives should be worth based on these formulas. Etc.

Yet, as Mandelbrot eloquently shows in the book, markets do not follow a Gaussian distribution. There are far too many wild swings than should be seen in a normal distribution. These swings, such as the 1929 stock market crash that kicked off the Great Depression, the 1987 Black Monday crash, the Tech Wreck, the 2008/9 global financial crisis — they simply shouldn’t happen if the markets were following a random walk with the volatility implied by a normal distribution. The standard models say that these types of events should be so rare as to be essentially impossible, like finding a human closing on the 10′ mark for height — basically, never in the course of human history should any of these events have happened, but there they are, and more that I haven’t listed, all within about one human lifespan. This volatility is, unfortunately, an inescapable feature of the markets.

Other core assumptions of the standard theories are also not true. For example, that price movements are independent. But, we know that volatility clusters. This is even something seen in nature, away from the madness of human market psychology: if you plot out the size of a river’s spring flood each year for hundreds of years, it will trace a nice bell-curve. If, using the information of that bell curve you were to make a dam so that, 99 years out of the 100 you expect the dam to last, the reservoir would be big enough to allow enough water to flow downstream to provide a water supply equal to the average spring flood, you’d find your dam would be too small. That’s because if the volatility clusters, it throws the calculations off. And that’s exactly what happens when you find that one dry year follows another follows another, while the wet ones cluster up together too — more often than should be happening if each was truly an independent event, as with games of chance in a casino.

Forgetting this assumption is one of the many factors that lead to the subprime crisis in the states. They had fairly decent models telling them how likely it was that someone with bad credit they were giving a mortgage to would default. These financial warlocks could then figure out how to tranche the loans out in a big securitization package so that the top tranche would not experience any defaults (and then later what interest rate they’d need to offer to get people to take a chance on the lower tranches). However, what they didn’t account for is the clustering of volatility — when the loans went bad, they all went bad at the same time.

And the third important way that real markets differ from our models of markets is that prices are not continuous. Many real physical things are continuous. It’s not possible for me to teleport my keyboard from the top of my desk to the floor. It must — however briefly — occupy each point along the height axis as it falls. Much of our mathematics is based on continuous functions. Markets, however, are not real, physical things. They are not continuous. However, the models assume that they are. For most retail investors, this is one of the less devastating distinctions from accepted theory: so what if prices take discrete jumps? For the fancy traders trying to limit risk though, non-continuity can break some of their techniques. One common one is the stop-loss order. You set a point at which you will not tolerate further drops in a stock’s price. If the stock is falling and hits your stop-loss price, it automatically gets sold by your broker. This can help you limit your downside.

But look at Manulife today. Let’s say a trader owned MFC and had a stop-loss set at $15.50, to limit their downside. This morning the results came out, and they were bad. The stock, which closed yesterday at $16 opened for trading today at $14.87. At no point was there ever an opportunity to sell it in the $15 range.

So, before I get off ranting about the concepts themselves, I’ll say that the book was very approachable, even if you don’t have much of a statistical bent. Mandelbrot uses graphs well to get his point across, and tries to keep things non-technical (and there is next to no math). However, it is a concept book — it’s not going to tell you how to build a better portfolio or manage risk better.

Now, having just spent some time discussing the idea that markets are more volatile than we thought, and that they are not efficient, what do I have to say?

Well, despite the volatility, for the long run the stock market has still been basically the best place to keep your money. In the short run, the volatility can be very painful (as we’ve seen recently). But, if you have many decades to wait, and believe that businesses will continue to be profitable, then you should get your money to work for you in the market. So, as someone still fairly young (despite my looks as science has ravaged my body), I have a very high equity allocation. However, despite agreeing in theory with the concept of lifecycle investing and using leverage while you’re young, I’ve never been comfortable with the idea in practice, and have never been very leveraged (and not at all at the moment).

Efficient market theory says that market participants are rational, have (roughly) equal access to information, and that information about past price changes does not enable you to predict future price changes. (The esoteric proofs of some of this rely on the normal distribution). This leads one to conclude that investing in index funds is the way to go, since beating the market is impossible. Now, I don’t believe in full efficient market theory. In particular, people are not rational, and all information is not widely and universally shared (or understood!). That’s why part of my investments are “actively” managed: I invest in particular companies I think have a good chance of beating the overall market. However that said, I do believe in a weaker form of efficient markets, which is that the average person can’t beat the market net of fees, so although I talk about my stock tips and analysis here on the blog for discussion and feedback, the only recommendation I ever give people who ask is to invest in a low-cost index fund, such as TD’s e-series funds or an iShares ETF (and part of my investments are in e-series funds).

Terence asked via email if I could comment on Garth Turner’s investment philosophy.

Garth of course is perhaps the most well-known real estate bear in Canada — it was his writing that lead me to look into the issue myself before potentially buying a house in 2006 (we ended up renting instead).

He also provides a bit of investing advice on his blog (and his book Money Road — which I have not yet read). He very often gets asked by readers (or “blog dogs”) what they should do with all the money they have if they do sell their house, or hold off on buying their first if they do have a downpayment. One of the things he recommends very often on his blog are preferred shares of the Canadian banks (and also insurers, utilities, etc) which pay in the neighbourhood of 5-6% these days, as a tax-advantaged dividend.

First up, what is a preferred share? It’s a bit of a strange beast that lies somewhere between a stock and a bond. You get a regular payout, like a bond, but it’s counted a dividend for tax purposes, like a stock. But, you don’t share in any upside of the company’s growth or progress, like a bond. Preferred shares fall between common equity (regular stocks) and bonds (and other debtholders) for getting paid back in a liquidation — something that is unlikely to be an important factor, as when companies do get liquidated these days, even the bondholders are seldom made whole, so the preferreds usually end up worthless as well (at least from what I’ve seen). The preferred dividend can, in hard times, be cancelled, but must generally be paid before the common dividend can be reinstated. As long as the company in question is doing moderately well, the preferred (and bonds) should continue to pay out, even if the common goes nowhere. Each preferred issue has its own set of rules, and even within one company there can be many series (often denoted with a letter) that play by different rules. Often they have a “par value”, a price at which the company will buy them back. Redemption though can be at the company’s option, not the holder’s.

All said, they typically offer a steady stream of income that is in-between a stock and a bond for riskiness, but far more tax-advantaged than a bond.

Now, there are several things to keep in mind when you see Garth recommending these things. The first is the audience: many people don’t think there is a way of getting more than 1% in a bank account or GIC without taking on the full risk of the equity market. He’s pointing out that there is something that will pay a consistent return — more return than many people are getting from the rent savings by owning their houses these days — and that will pay it similar to how a GIC/HISA pays out, i.e. fixed and regular, without the uncertainty of return that’s inherent to capital appreciation. Also, the audience tends to be either baby boomers who need income for retirement (or to pay the rent if they sold off their nearly-paid-for houses), or newbies who don’t know that there are ways to get their money working in a relatively low-risk way.

Related to that is the idea of tax efficiency: for someone with nearly no income (a grad student like me) or lots of tax shelter room, finding a bond at 5.5% is equivalent to a preferred at 5.5%, so why not go with the bond since it’s a little safer? But for someone in a higher tax bracket, who just sold a paid-off house, that preferred at 5.5% may beat out a bond at 8% due to the tax advantage.

Also, it’s a rhetorical device: as I said above, it’s a good example of a way to make a decent return to someone that doesn’t know anything beyond “the dutch guy’s shorts.” He’s not recommending that people buy only preferreds, but since it’s one of the less-discussed options (stocks and bonds get hundreds of times more thoughtspace and attention than preffereds do) it makes it worth talking about, both because it gives him a somewhat unique message, and because it helps educate his audience. When he does give investment advice on the Greater Fool blog, he’ll spend most of it talking about preferreds (or rather quipping one-liners about preferreds), but he’s not by any means recommending that people only buy preferreds.

Finally, Garth’s outlook is that the overall market will be choppy but generally flat, if I’ve read his message right, so he doesn’t see much of a risk premium for stepping up from preferreds to commons. If that’s your viewpoint, then locking in a mid-5% return is quite good. Vice-versa, the spread between a company’s debt and preferreds are quite high right now, also indicating they may be worthwhile, though I’m having trouble finding out what the historical spread was.

Terrence also asked about the interest rate sensitivity, pointing out that preferreds may have been a good investment recently because interest rates have gone down (similar to bonds, preferred prices go up as rates go down). Now, these will have some interest-rate sensitivity, and due to the perpetual nature of many (the company calls them back for redemption rather than the holder), you get a little less protection than a bond (which can be held to maturity). However, if you don’t have to trade them, then the changes in the price is not too much of a concern, and being able to lock in today for a ~5.5% dividend is not too shabby, considering 5-10 year bonds from the same banks are only in the 3-4% range right now. If you do need to sell within a few years, then you can get hurt by the fluctuations in price. One note though: due to not knowing when a preferred will get called, there’s the concept of “yield to worst”. If you buy a preferred with a high coupon, that is, after interest rates had dropped, so the price went up, the redemption price the company can call it at is still say $25. So if you paid $26 and are getting some quarterly payment as well, your yield to worst would be lower than the cash yield since the company could call the preferred back at $25, giving you a $1 loss at the end. Another risk to watch out for when talking about changing interest rates and buying/selling preferreds.

So all that said, what do I think? Well, I think for the target audience, they’re a great investment vehicle. But for my audience, which is typically younger, they’re not really worth looking into. If you’re a little older and starting to become more conservative in your risk tolerance, and also wealthier, then they can be great: as you shift more towards fixed income, you may very well want to subdivide your focus to spread out amongst a 5-year bond ladder, some longer bonds, some corporates, some real return, and of course, some preferreds. For a younger, poorer audience, with higher risk tolerance, I figure fixed income should be a fairly small portion of the portfolio, and what fixed income there is should be ultra-safe (HISA/GICs/Government bonds) since it’s function is to be the security blanket, or the money needed in the near-to-middle term that can’t be put at risk — and there likely won’t be enough fixed income to make it worthwhile sub-dividing the category so finely.

The added complication of each series having its own rules on redemption, dividend payout adjustments, etc., also means there can be a lot of reading involved for a fairly illiquid instrument. There are some preferred ETFs that can help make buying some easier, but still, I don’t see the point for someone who’s got decades of time to get the rewards promised in common equity.

That said, just ’cause you’re young doesn’t mean you have the same risk tolerance I do (and there may be older folks amongst our readers too!) so if anyone out there is interested in learning more about preferreds, feel free to ask any questions and I’ll try to help out!

I’ve had about 5 hours of sleep in the last 48 hours as I try to cram out (at the last minute, of course) some papers for an upcoming conference. It’s been a nightmare because, amongst other reasons, the ridiculous copyright policy of the conference means that we have to submit papers that are different enough from what we usually write that we can still have freedom to use our own work elsewhere. It’s hard enough to hammer out a paper in the first place, then to have to try to do it in the literary equivalent of a funny accent…

Anyhow, I’ve been battling with yet another nasty case of writer’s block — something that seems to hit me far too severely when it comes to my professional writing. I think Wayfare hit the issue on the head: I worry too much about how the work will be received for professional stuff and just lock up, whereas on my pseudo-anonymous blog I can just hammer away at the keyboard and not even worry about proof reading since I don’t have that much invested in it. Nothing to do but just try to get over it. In the meantime, Netbug suggested I take a quick break and put up at least a Tater’s Takes post, so here you go.

On the health/diet front, I found out that my scale got miscalibrated somewhere along the way. I’m not sure when it happened, but it was reading high by 3-4 pounds, which means I’ve really only gained about a pound from when I started. Still, wrong direction, but not quite as bad as I had thought. The last week was decent but not great: I’ve been watching what I eat more, but still had a few doughnuts at work through the week. I’ve started writing down my meal plan for a ~3 day period, and have been sticking to it reasonably well, and including lots of healthy stuff like vegetables and oatmeal, so that’s been good. I only had two good long bikerides in the week, but considering the week I’ve had, that’s pretty good (I plan on retrying the 36 km trip around Fanshawe Lake once these stupid stupid stupid papers are in).

“Today” though has been hell on the diet: I’ve resorted to undergrad cram tactics, pounding down full-sugar Coke & Red Bull and eating nothing but junk food to burn through the night. 3940 calories in the last 24 hour period (I don’t know what I consider a “day” anymore — best to try to stick to the subjective view of time the rest of you hold), which is simply not an efficient way to produce written words. As soon as the caffeine starts to wear off, I’m right into the head-bobbing vertigo stage of sleep deprivation, so I’m really hoping these stupid papers get finished soon.

In the news, BP’s latest cap attempt actually appears to be working. The stock shot up, then slid back down on perhaps fears that the shutting-in of the oil may have put too much pressure on the parts of the well below the ocean floor, causing oil to seep out (in a way that could be very difficult to control).

Also finance-related, a quick note that I sold my H&R REIT yesterday. Thanks to falling behind on my thesis and staying a grad student longer than my scholarship said I should I know that I’ll need to be raising cash, and also H&R is starting to look fully valued to me, so out it goes. Again, this isn’t a case of not liking the company, just thinking that the price was getting high enough…

After running headlong into Bell’s very restrictive 25 GB data cap in May, I had to complain to any that would hear me that the $2/GB charge was very obviously excessive, and in no way actually reflected the incremental cost of that data usage. Plus, of course, the comparison to Rogers’ slightly more generous 60 GB cap (and 5 years ago the cap was also 60 GB, long before most users started watching videos on the internet, or Bell/Rogers themselves started rolling out video-on-demand portals). Netbug sent along an article that looks at this issue for US ISPs and concludes that indeed, most of the cost structure is composed of fixed-cost infrastructure type spending, and there’s no support in the ISPs’ business model for the caps and data charges that have been rolled out. Congestion issues are also unlikely to be the reason for the fees, since if congestion at peak times was the issue, the ISPs should instead implement time-of-use charges.

Questrade: ETFs are free to trade, and if you sign up with my link you'll get $50 cash back (must fund your account with at least $250 within 90 days).

Questrade: ETFs are free to trade, and if you sign up with my link you'll get $50 cash back (must fund your account with at least $250 within 90 days).  Passiv is a tool that can connect to your Questrade account and make it easier to track and rebalance your portfolio, including sending you an email reminder when new cash arrives and is ready to be invested.

Passiv is a tool that can connect to your Questrade account and make it easier to track and rebalance your portfolio, including sending you an email reminder when new cash arrives and is ready to be invested.