The Idea of Risk and the Housing Bubble

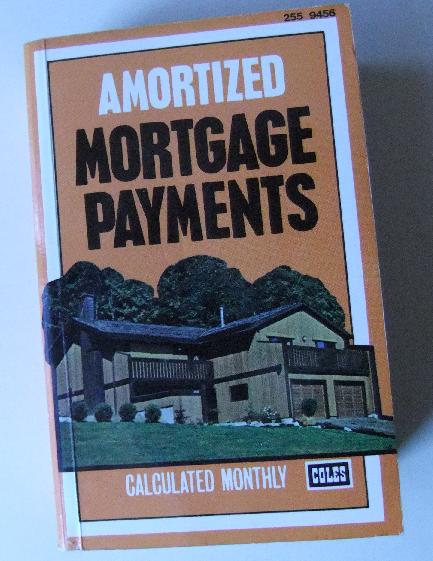

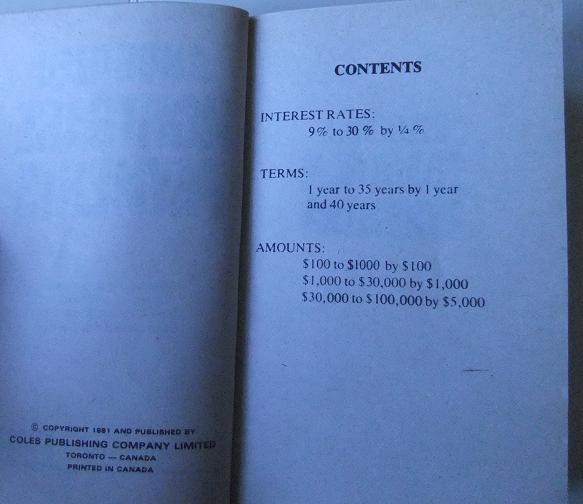

January 8th, 2011 by PotatoPartly for the laugh, Wayfare gave me a book of mortgage payment tables for Potatomas. For those of you not familiar with these tables, they date from a time before spreadsheets and online java calculators, when if you wanted to know what the monthly payment on a mortgage of a certain amortization at a certain interest rate would come out to, you had to run the calculation by hand. To help, tables were drawn up with the figures pre-calculated so one could just look up the value rather than calculating it. It was published in 1981, and has tables for 9% interest through 30% interest, in 25 bp increments. Interest rates below 9% were so unfathomable that they didn’t bother to print them in the book.

I’m not sure what the lesson there is: whether these current low interest rates are indeed so far below the historical norm that people should be prepared for higher rates in years to come, or the opposite: that times change, and now 9% is unfathomably high, and I shouldn’t keep trying to warn people about rates that aren’t likely to be seen again.

Anyhow, I wanted to explore a little bit the idea of risk and the housing bubble. This is based a bit upon some percolation of recurring themes here, and a bit upon some things people are saying on the internet (because no one in real life wants to talk to me about housing anymore).

First we really have to try to understand risk. Everyone has at least a little bit of gut feel for what risk is, and how some things are riskier than others. But everything has some form of risk to it: even GICs risk not keeping up with inflation, or in large concentrations, outliving your money. Volatility is sometimes used as a proxy for risk, in part because it’s easier to measure. But volatility doesn’t tell the whole story of risk, not by a long shot. If I’m talking about risk being the potential for permanent loss, for turning your life inside-out and just ruining your whole day, then volatility isn’t really a good measure of that at all.

If you look at a graph of the Toronto housing market over a number of years, it’s this incredibly smooth line moving up from the late 90’s to the late 00’s, and even beyond that there’s this smoothed bump in the 80’s and a little wiggle at the end in ’08/’09. So in terms of volatility, housing doesn’t look risky at all. Yet to my mind, it really is. One part of that is how the lack of volatility works against it when there is a crash. Go back to the last crash in ’89. If you were unlucky enough to buy at the top there, you’d see the value of your home decline some 30%, and stay down for years. It would take well over a decade to get back to break-even.

“But,” the people say, “why would I sell then?” And that’s a very strange question, because those same people often don’t have the same pragmatic zen attitude towards stock market corrections. With housing, you can be forced to sell when you’re underwater, for the usual reasons: job loss, move, family circumstances change, etc. When the stock market crashes though, you don’t have to sell your stocks (except for margin calls), unless you’re already retired. Heck, you can even rebalance and buy more.

The stock market by comparison is far more volatile, on any timescale. There have been 3 separate crashes in the Toronto stock market since the 1989 Toronto housing market crash. And the severity can also be frighteningly worse, about 50% top-to-bottom in the last crash. But, the recoveries are far snappier: not even counting dividends, someone unlucky enough to invest at the very peak of the market in 1989 was made whole by what looks* to be 1993; someone concerned with getting back to the 2000 peak found it in 5 years. Though we haven’t quite gotten back to the peak of mid-2008, in just 2.5 years we’re down less than 10%, and I’m pretty sure another 2.5 will find us back up there (and that’s not including dividends). Yeah, stocks are more volatile, but that works both ways, which means those crashes are both more frequent but also transitory. And you don’t have to buy in one chunk and get unlucky and find yourself at the peak (like with a house) — you can buy in year after year, so the real-life situation isn’t even this dire (as one would hope, since your investments are supposed to make you money). With diversification and rebalancing, you can do even better than the straight index.

But there’s still the fairly legitimate idea that stocks are risky: they can go to zero. Nortel went to zero, and that event seems to be burned into the Canadian mindset. “Can you point me to the house that went to zero?” Well, individual stocks are risky, but portfolios much less so. Even in one of the worst stock market declines in recent memory, a diversified portfolio was only down by about half, and much less if you had bonds too, and even then only for a short period of time. Think not so much of the house that went to zero, but the roof, or waterheater, or deck that became worthless. They’re just components of the overall investment, which as a whole is not as risky as the sum of its parts.

Leverage and familiarity of course play into the real and perceived risks: because of the high leverage employed these days (5% down baby), I’m deathly afraid of the potential for real estate to ruin your whole life. Because it’s strange and foreign, people in general are afraid of equities: the concept of distributed ownership in hundreds of companies is alien, and not in the daily experience of most people (or even in their educational readings), but everyone knows about houses (in fact, I’m writing this rant while sitting in one). However, the lack of volatility, and the last crash taking place when my cohort was still in elementary school can lead to some false complacency on the matter.

I’ve mentioned before that if real estate is overvalued by 30%, and if the typical family spends about 30% of their income on housing, then if they buy in too close to that peak, that leads to about 10% less money in the budget — about what people save for retirement. Even though it’s not so expensive that you can’t afford to put a roof over your head (that would probably bring an end to the bubble), it’s pricey enough to impact your financial health for essentially the rest of your life, which is why I waste so many electrons on this. It’s legitimately important, and it can be controlled.

I don’t know how to get people comfortable with stocks though, because it’s a fair point that if you don’t save and invest the difference when renting, the benefit isn’t really there (though even just saving in a savings account may be attractive if housing is overpriced enough relative to rent). On the one hand, equities are the riskiest, most volatile class of investments. Indeed, Mandelbrot suggests they may be even riskier than we first imagine. On the other hand, they’re not all that risky when diversified and held for very long periods of time (and as youngish folks, we have very long periods of time on our hands). Combined with the fact that it’s cheaper to rent right now, renting and investing the difference really looks to be the less risky path. Though the English language has the expression “safe as houses”, it’s not true all the time, and blind faith in real estate is in my mind, one of the most risky notions facing young Torontonians and Vancouverites.

* – Sorry, I just have a (not particularly great) graph for data that old.

Questrade: ETFs are free to trade, and if you sign up with my link you'll get $50 cash back (must fund your account with at least $250 within 90 days).

Questrade: ETFs are free to trade, and if you sign up with my link you'll get $50 cash back (must fund your account with at least $250 within 90 days).  Passiv is a tool that can connect to your Questrade account and make it easier to track and rebalance your portfolio, including sending you an email reminder when new cash arrives and is ready to be invested.

Passiv is a tool that can connect to your Questrade account and make it easier to track and rebalance your portfolio, including sending you an email reminder when new cash arrives and is ready to be invested.